what is the yield to maturity for bed bath and beyond long term debt

While shares of Bed Bath & Beyond (NASDAQ:BBBY) have performed remarkably well since Apr, upwards over 250%, the long term signals that its bonds were flashing nonetheless remain. Fifty-fifty though Bed Bath & Beyond is working to revitalize its digital side, it doesn't seem to have the necessary majuscule structure to keep itself afloat in the long-term swing of things.

When I final covered Bed Bathroom & Beyond on Apr 1 (read here), it was quite difficult to see how the retail surroundings would transform. Bed Bath & Beyond closed over ane,300 stores, merely was committed to keeping its Harmon and buybuyBaby stores open up to provide infant essentials. CEO Mark Tritton best-selling that Bed Bath & Beyond was in a financially stable position with over $i.iv billion in cash and access to credit facilities.

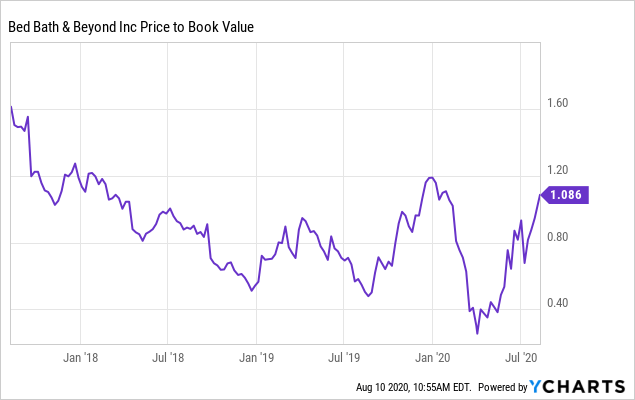

Back so, Bed Bath & Beyond looked promising from a short-term recovery standpoint when information technology had been floating effectually $4 per share, since it was trading at a P/B of ~.30. Then, while the whole retail industry was still reeling from firsthand shocks (closures) and defalcation fears were heightened, Bed Bath & Beyond, like many retailers, was trading far beneath its book.

Now, Bed Bathroom & Across is trading at a P/B of ~1.07, per its book value of $11.75 calculated from its nigh recent quarterly results. It's a chip troublesome that while the business organisation dynamic has shifted from in-shop to online, Bed Bath & Beyond is pushing towards valuations on a P/B standpoint it last saw in late 2019, and early 2018 when information technology had been posting quarterly profits.

Information by YCharts

Information by YChartsWhile Bed Bath & Across looks less highly-seasoned from its P/B than it had in April, its bonds nonetheless show a promising outlook. Bed Bath & Beyond has posted half dozen straight quarters of net losses , variable greenbacks flows, and $250 million more debt added during last quarter, which could make its access to credit harder in the long term.

Moody's ratings on the three long-term bonds - 2024 maturity, 2034 maturity, 2044 maturity - take dropped to B1 as of July 23, whereas the three were previously rated two steps higher at Ba2. That puts the bonds in the 'highly speculative' bracket as opposed to 'not-investment grade speculative'. Any other rating drops to B2 or B3 would put the bonds on the brink of a C rating, with substantial risk of default.

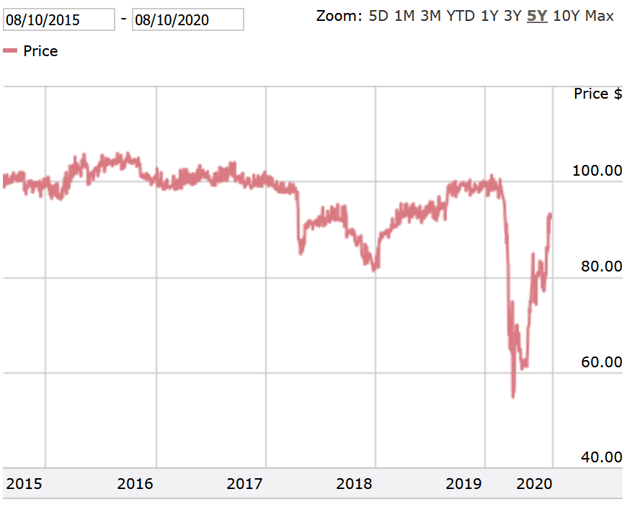

The 2024 maturity final traded at $91.80, a substantial gain since April 1'southward merchandise price of $threescore.78. While the bond dipped downwards to beneath lx cents on the dollar, it has recovered quite well, trading above late 2018's levels in the 80s. There's non much fearfulness anymore of an imminent bankruptcy to Bed Bathroom & Beyond.

Source: FINRA (bond information linked above)

Source: FINRA (bond information linked above)

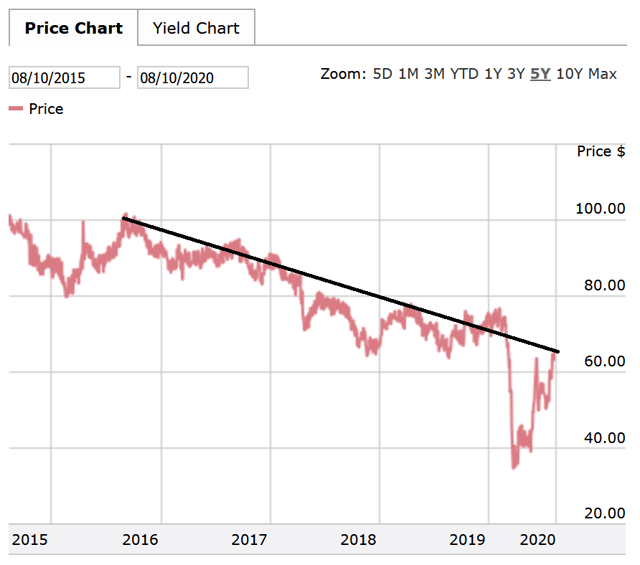

The later maturing bonds are where worrisome trends start to ascend. Again, while both have shown a solid recovery since April, the overall trend in bonds' prices since 2015 take been quite consistently negative, signaling less and less hope of a full-out recovery for those creditors.

The 2034 maturity terminal traded at $lxx.01, barely higher up tardily 2018's prices, but far from where information technology had fallen in April, at 39 cents on the dollar. While that recovery is quite astounding, the bond has non recovered enough past its general trendline to fuel hopes of a long-term recovery. The price of the bond correlates with the downgrade in rating, as 'highly speculative' starts to betoken signs of distress, which is typically denoted by bonds trading at 60 cents or less on the dollar. While the 2034 maturity is trading just above that level, its long-term trend would have it trading at 'distressed' values within 2 years.

Source: FINRA (bond data linked to a higher place, trendline added)

Source: FINRA (bond data linked to a higher place, trendline added)

The case is the aforementioned with the 2044 maturity; information technology concluding traded at $63.xv, after falling to just about 35 cents on the dollar in April. The trendline is almost identical between the two bonds. Nonetheless, since this bail is a later maturity, it is trading much closer to that 'distressed' threshold, and could be trading below 60 within a year.

Source: FINRA (bail data linked above, trendline added)

Source: FINRA (bail data linked above, trendline added)

The two later maturing bonds contain the bulk of Bed Bathroom & Beyond's long-term debt - with $1.75 billion total outstanding, $1.2 billion of that is due between the 2034 and 2044 bonds (with $300 one thousand thousand and $900 million outstanding, respectively). With that in mind, Bed Bath & Beyond will have interest expenses on these two for a long time to come up.

Bed Bathroom & Beyond has about $ane.i billion in cash on hand, and looks to have navigated the original downturn quite well. It is taking initiatives to narrow its business organization - "reviewing its not-cadre avails to focus on optimizing growth opportunities within the domicile, baby, beauty and health categories" to potentially unlock nearly half a billion in value, and to piece of work on further capitalization of "an fourscore% increase in digital channels." Online shopping with ii hour store pickup and curbside pickup will be added to its holiday shopping flavor.

While those are certainly positives for the short term, it seems doubtful that Bed Bath & Across's $1.1 billion in greenbacks is enough to revitalize itself in the face of a larger trend towards e-commerce among rising contest from Wayfair (Westward) and Overstock (OSTK) in the abode aqueduct, as well every bit from giant Amazon (AMZN), among others. Bed Bath & Beyond is still a small fish in the e-commerce pond, and those much bigger fish have significantly better infrastructures (i.e. shipping/distribution facilities) to support growing digitization trends peculiarly as the holiday season ramps up in a few months. If Bed Bath & Across wants to transform itself digitally at some bespeak in the futurity, $1.1 billion is not nearly enough to do so at scale.

Every bit bonds continue down the path towards a less hopeful recovery, trading between 60 and seventy cents on the dollar, Bed Bath & Beyond needs a catalyst - information technology looks to be coming down to how that cash is spent. It could be used to revitalize and upgrade stores, or expand a footprint, which might not do good the company equally much in the face of growing digital sales, or information technology could work on expanding efforts digitally and upgrading that segment, amid risks of heightened competition in the due east-tail infinite.

Only that capital outlay needs to have a return, as Bed Bath & Across can't go spending its greenbacks reserves to undergone scenarios similar that if information technology won't have earn enough of a return to pay off its debts. If information technology does undergo some scenario similar that, and needs to starting time making advances to acquire new debt, it could be significantly harder to acquire either a large sum, or a sum at a favorable interest rate given its credit ratings right now.

All in all, the challenges facing Bed Bath & Across in the digital realm and the physical realm in the long term volition likely require a significant capital letter outlay, one that could further pressure the company. Its 2024 bond has recovered quite well in the face of a challenging year, simply its subsequently maturing 2034 and 2044 bonds are nonetheless continuing on the downtrend in place since 2016. When shares were consistently trading beneath volume value throughout 2018 to mid-2019, the long-term bonds were trading significantly higher, near 80 cents on the dollar. As bonds are falling even so, Bed Bathroom & Across looks to have less upside to a higher place book value - with bondholders in the long-run notwithstanding slowly losing organized religion in a recovery, investing in Bed Bath & Beyond now, at over its book value, looks far less highly-seasoned from a risk/reward standpoint.

This article was written past

BA Concern, 21 years old. I've been investing for 10 years and so far, and take extensive background in technical assay and event driven movements in stocks, such equally earnings and momentum. Most of my coverage will exist unmarried disinterestedness focused in tech/EV, consumer discretionary, and emerging market equities, aided with some macro/behavioral/strategy pieces.

Disclosure: I/we take no positions in any stocks mentioned, and no plans to initiate any positions inside the next 72 hours. I wrote this article myself, and it expresses my ain opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business human relationship with any company whose stock is mentioned in this article.

Source: https://seekingalpha.com/article/4367508-bed-bath-and-beyond-not-really-promising-long-term-prospect

0 Response to "what is the yield to maturity for bed bath and beyond long term debt"

Post a Comment